HealthCare Appraisers has observed an uptick in activity and interest in the home health and hospice space. This article provides background information on the home health and hospice industries, and then provides insight into what is driving the increased interest from healthcare providers as well as investors. We provide a discussion of the outlook for the industry, including how the recently implemented PDGM reimbursement model is likely to affect the provider landscape, as well as the impact of telehealth. We then discuss the approaches to value and how they are applied to home health and hospice business valuations.

![]() BACKGROUND

BACKGROUND

Home healthcare is the provision of medical care in the patient’s home following an injury or illness. The patient’s home can range from personal residence, skilled nursing facility, assisted living community, or wherever the patient calls home. Common home healthcare services include patient monitoring, medication management, assessing patient falls, palliative care, identifying diet and nutritional deficiencies, observing mental health, patient education, and functional support such as dressing and feeding patients. In order to qualify for Medicare reimbursement for home health services, the patient must be unable to leave their home without considerable effort, and must require part-time or intermittent skilled care, as certified by a physician. Hospice is a type of healthcare that provides comfort to patients with a prognosis of less than six months to live. In many cases, hospice is provided in a home setting as a type of home healthcare.

Home healthcare agencies consist of a variety of types of providers and non-providers including nurses, therapists and social workers, and care is coordinated with the patient’s physician. Hospice care is provided through many of the same types of providers as home health but can also include religious or spiritual counselors and bereavement specialists. Hospice care can also include services outside of traditional medicine including animal and music therapy.

![]() SIZE OF THE MARKET

SIZE OF THE MARKET

As of 2017, there were approximately 3.4 million Medicare beneficiaries receiving home healthcare services, and 1.49 million Medicare beneficiaries receiving hospice services. The number of providers in the home health and hospice sector has been steadily increasing since the year 2000. In particular, the number of home healthcare agencies increased from 7,528 in the year 2000 to 10,785 in 2018. The number of hospice providers increased from 2,255 to 3,864 over the same time period.[1] Much of the aforementioned increase has been for-profit entities.[2]

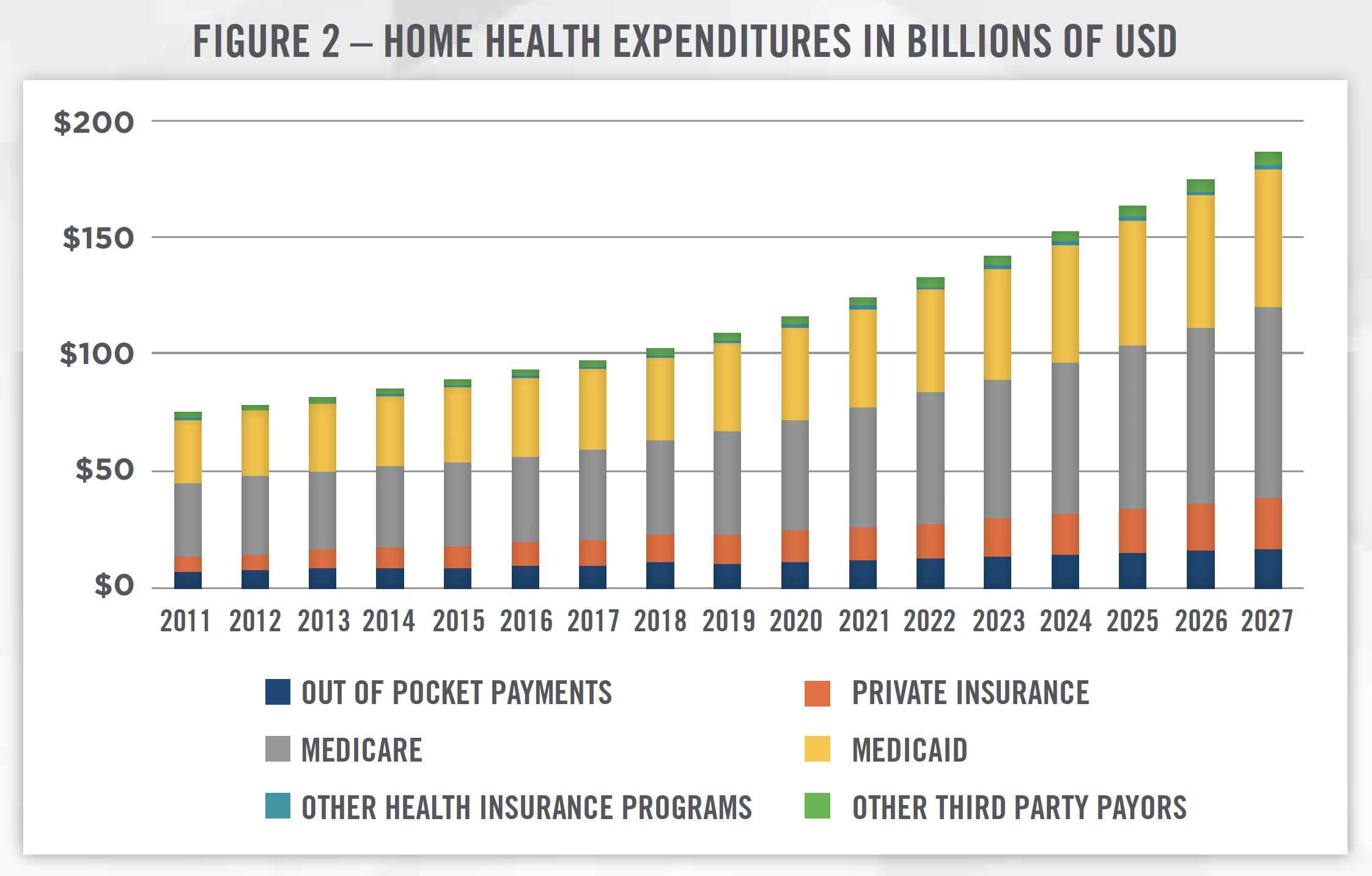

According to CMS, total expenditures for home healthcare[3] in 2018, the most recent year for which data was available, was $102.2 billion. Home healthcare expenditures have increased approximately four to five percent per year for the last several years. Figure 2 presents home health expenditures from 2011 through 2018, as well as projected expenditures through 2027. CMS projects home healthcare expenditures to increase approximately seven percent per year through 2027.

There are many growth drivers impacting the increase in home healthcare expenditures in the United States. Major factors include the aging population, the shift to value-based care and recognition by providers and payors that home healthcare can help reduce readmissions, and the overall push to control costs within the healthcare system. In particular, home healthcare is increasingly being utilized to keep elderly patients in their homes as opposed to assisted-living communities. Home healthcare providers are also being used as an alternative to primary care physicians, and this trend is expected to accelerate as the shortage of primary care physicians is anticipated to worsen in the coming years.[4]

![]() REIMBURSEMENT

REIMBURSEMENT

Until recently, Medicare reimbursement for home healthcare services was based on 60-day episodes of care. Medicare sets the base rate for a standard 60-day episode, then payment for each episode is adjusted upwards or downwards based on the patient’s clinical and functional needs, as well as the patients expected utilization of services. Prior to implementation of the Patient-Driven Groupings Model (“PDGM”) in 2020, there were 153 payment groups into which patients could be classified that determined the adjustment to the base rate. In 2019, the 60-day episodic base rate for home healthcare services was $3,154, up from $3,040 in 2018. Due to the long timeframe during which care was provided, providers could submit Request for Anticipated Payment (“RAP”) to CMS, and receive up to 60 percent of the anticipated reimbursement up front, with the remainder received at the end of the episode.

Beginning in 2020, the implementation of PDGM will reshape how home healthcare services are reimbursed and will likely have a dramatic impact on the home healthcare landscape in the coming years (discussed in more detail in later sections). Under the new payment model, the number of payment groupings is increasing from 153 to 432 and are classified based on episode timing, referral source, clinical category, functional/cognitive level, and presence of comorbidities. CMS is also phasing out RAP for new providers in 2020 and for existing providers in 2021. The increasing complexity of the payment model and associated coding and billing requirements, as well as the elimination of RAP, is expected to increase costs for providers, particularly smaller agencies, and lead to a period of consolidation within the industry.

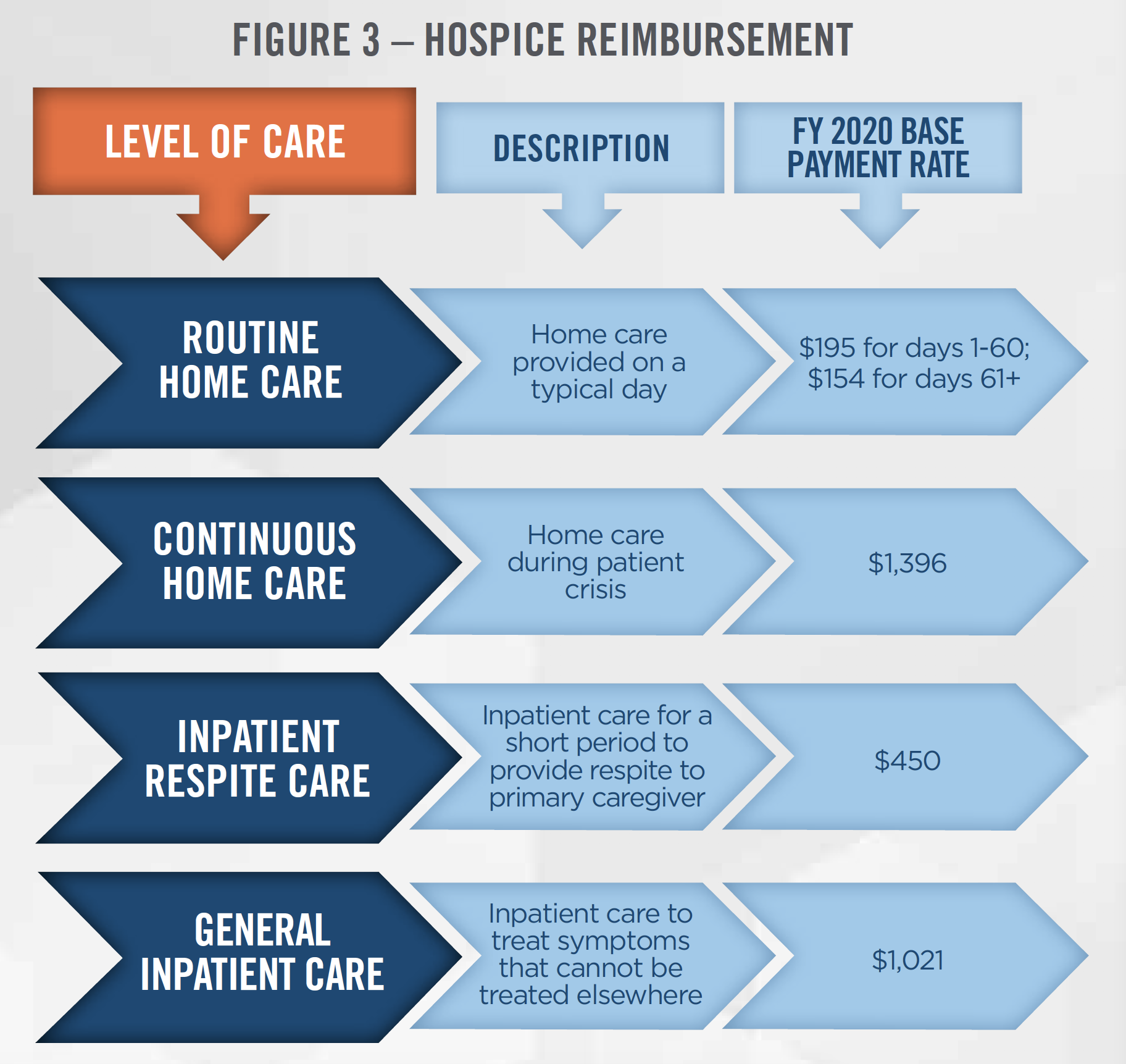

Hospice reimbursement is based on a daily payment rate that is determined according to a fee schedule depending on the level of care provided. There are four levels of care that can be provided under the hospice Medicare benefit, each with its own payment rate. The most common is routine home care, which accounts for 98 percent of all hospice days and has a 2020 payment rate of $195 per day for the first 60 days, and $154 per day thereafter. The four levels of care and the associated base payment rates are presented in Figure 3.[5] The base rates are then adjusted to reflect different labor costs in different geographic locations throughout the United States.

![]() COMPETITIVE LANDSCAPE

COMPETITIVE LANDSCAPE

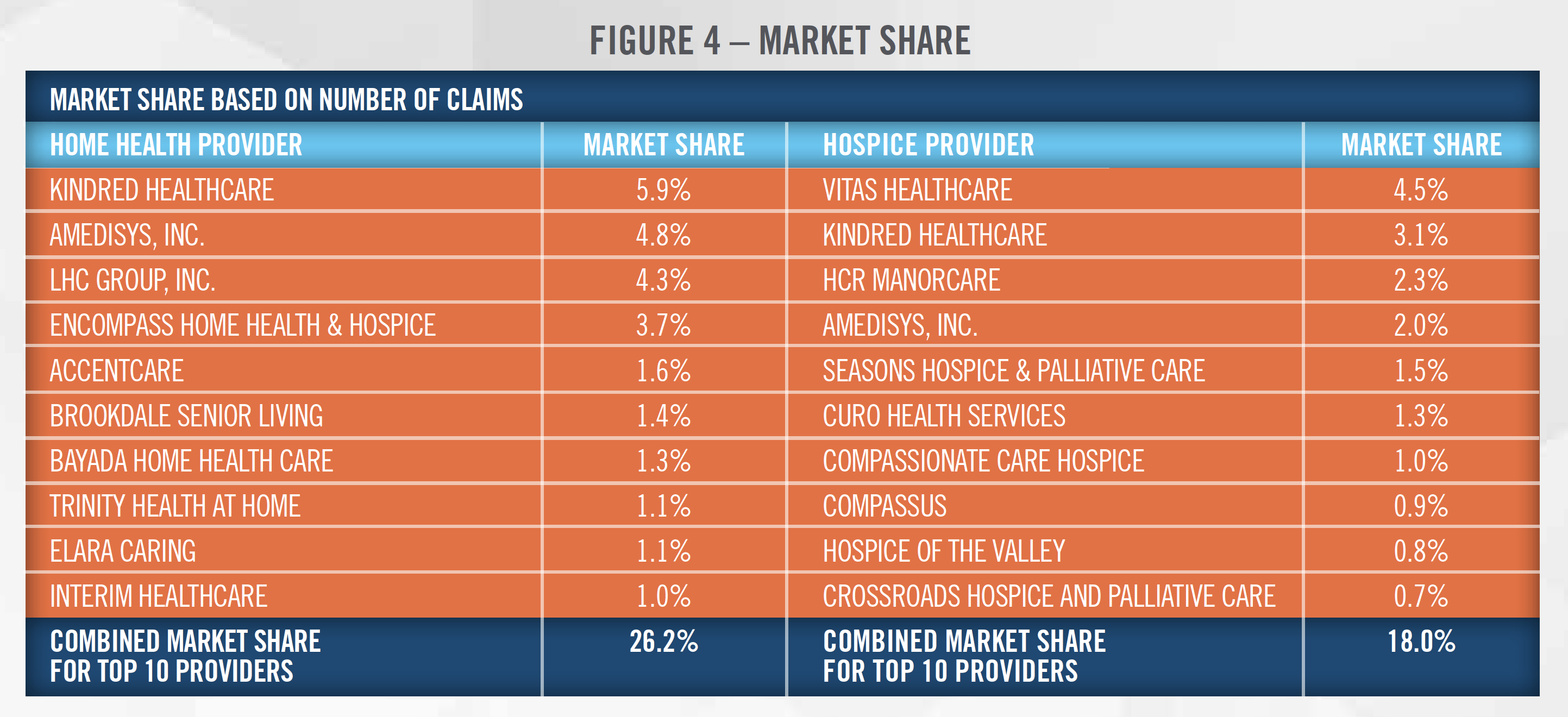

While there has been steady transaction activity in the home health and hospice market in recent years, the market remains relatively fragmented. As presented in Figure 4, the top 10 home health providers represented 26.2 percent of the national market share, while the top 10 hospice providers represented 18.0 percent of the national market, based on claims data as of 2019.[6]

Many of the largest operators in the country are publicly-traded corporations deriving some portion of their revenue from the provision of home health and/or hospice services. In particular, Kindred Healthcare offers both home health and hospice services, and was part of a transaction which combined its home health business with Curo Health Services before being acquired by Humana and two private equity investors. Amedisys, LHC Group, Encompass, Brookdale Senior Living, and VITAS (subsidiary of Chemed Corporation) are all publicly-traded corporations. In addition to the public operators, many of the largest home health and hospice platforms listed above are backed by private equity sponsors.

![]() OUTLOOK

OUTLOOK

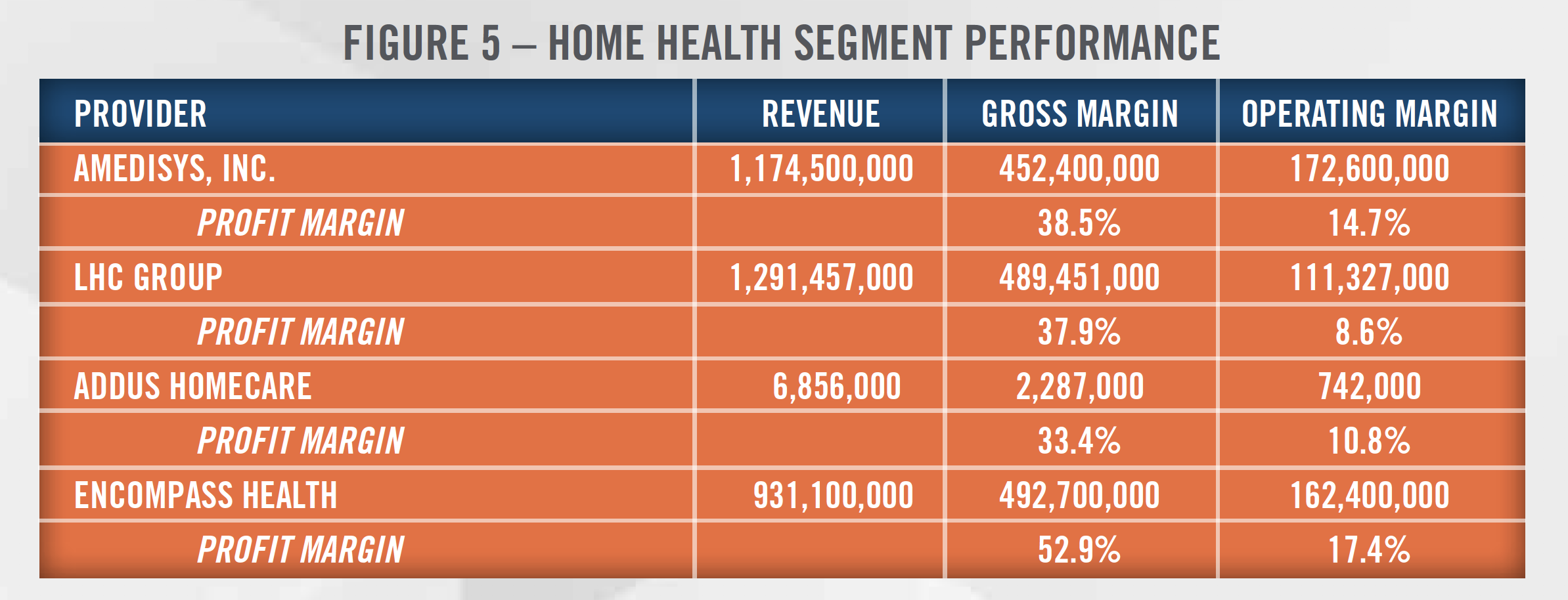

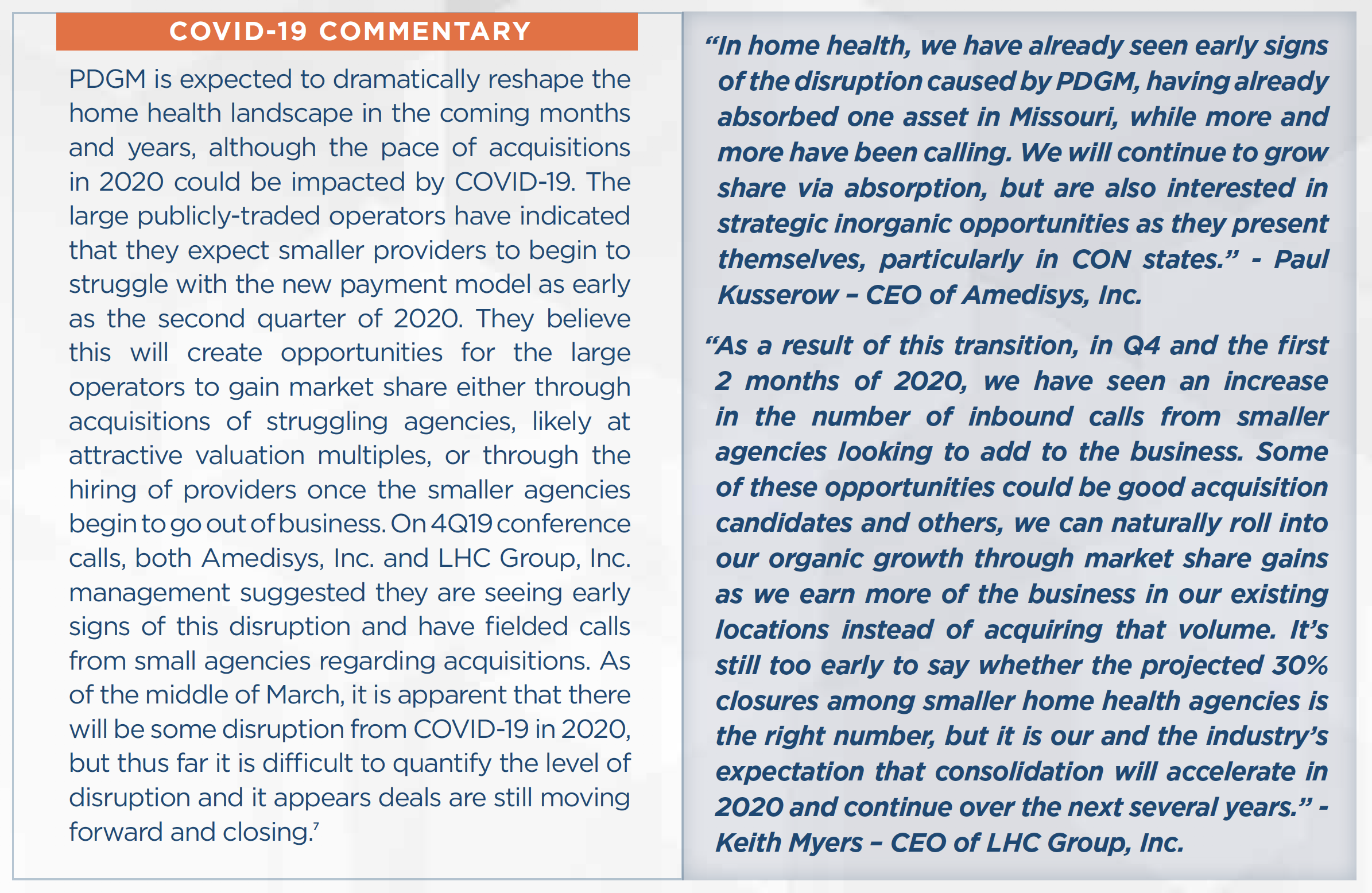

Heading into 2020 and beyond, industry participants expect a wave of consolidation as smaller providers are acquired either by large publicly-traded operators or private equity sponsored organizations. The main driver of this expected wave of consolidation is the implementation of PDGM, which cuts overall reimbursement rates, increases the complexity of coding and billing, and phases out RAP, all of which are expected to disproportionately impact smaller providers who may not have the resources to adapt to the new payment model. In particular, the phase out of RAP will increase the cash conversion cycle for providers and lead to higher working capital requirements. In order to properly code and bill under the new system, providers may need to hire dedicated staff members or consultants that understand the new payment groupings, which may increase expenses for the agencies. In addition, smaller agencies are generally less profitable than larger operators, with all-payor margins for home health agencies of 4.5 percent as reported by MedPac for 2017. This compares to the considerably higher profit margins reported by the public companies. Figure 5 presents home health segment gross profit margin and operating profit margin for some of the largest providers in the space for 2018.

COVID-19 COMMENTARY

COVID-19 COMMENTARY

Acquisitions of struggling agencies are frequently based on asset-value, and we discuss valuations for these types of transactions in later sections.

Another side effect of the PDGM is the expected layoffs of therapists by home health providers due to changes in the way that therapy services are reimbursed. Beginning in 2020, therapy services will no longer be reimbursed on a per visit basis, but will be reimbursed based on the patient’s clinical characteristics and the complexity of the patient’s needs. As a result, home health operators are expected to (and in some cases already have[8]) lay off therapists as utilization of these services is expected to decline. In order to gauge the magnitude of the potential layoffs of therapists in home health, some industry participants have drawn parallels to the recently implemented Patient Driven Payment Model in the skilled nursing space which caused dramatic layoffs in the first few months of implementation.

The outlook for hospice may also be impacted by upcoming changes to the reimbursement landscape. In 2021 CMS is piloting a program through its Value-Based Insurance Design model that enables Medicare Advantage plans to cover hospice. Currently, the hospice benefit is covered by Medicare only, and the aim of the new program is to provide better coordination of care for Medicare Advantage beneficiaries. Some industry participants believe the ability for hospices to be reimbursed by Medicare Advantage plans could open the door to increased investment from private equity sponsors. This could lead to increased transaction activity and higher valuation multiples for such hospice providers.

In addition to new payment models, innovative new partnerships are forming throughout the home health and hospice industry. The acquisition of Kindred Healthcare’s home health and hospice business by Humana gave Humana the largest home health and hospice provider in the United States, and better positioned the insurer to provide value-based care. Other insurers, including UnitedHealth Group through its Optum platform, have similar home health capabilities. Walmart also recently partnered with Amedisys to provide home health services through its Walmart Health clinics, as Walmart continues to expand the number of services provided to patients through its in-store clinics.

COVID-19 COMMENTARY

![]() VALUATIONS

VALUATIONS

The three most common valuation approaches, the income, market and cost approaches, can all be applied when valuing home health and hospice businesses. The income approach values businesses, interests in businesses, or assets by converting future expected economic benefits into a present dollar amount using a risk-adjusted rate of return. According to data from MedPac, both home health and hospice providers have positive margins, on average, suggesting that these businesses are profitable and that an income approach is frequently an appropriate approach to consider. It is important for valuators to understand how expected changes in the industry impact the outlook for the business being valued. For example, reimbursement rates for home health providers are expected to decline in 2020 under the new payment model. In addition, the mix of services provided by home health agencies will likely shift as therapy utilization is expected to decline based on changes to how these services are reimbursed by CMS. The phase out of RAP will eliminate the ability of home health agencies to finance operations with payments received prior to the provision of services. Agencies will therefore have to keep more cash on hand to fund operations. Accounts receivable will also likely increase as a result of the RAP phase out. More broadly, uncertainty surrounding the future of many smaller home health agencies could lead to higher discount rates applied to the projected cash flows and, as a result, lower valuation multiples.

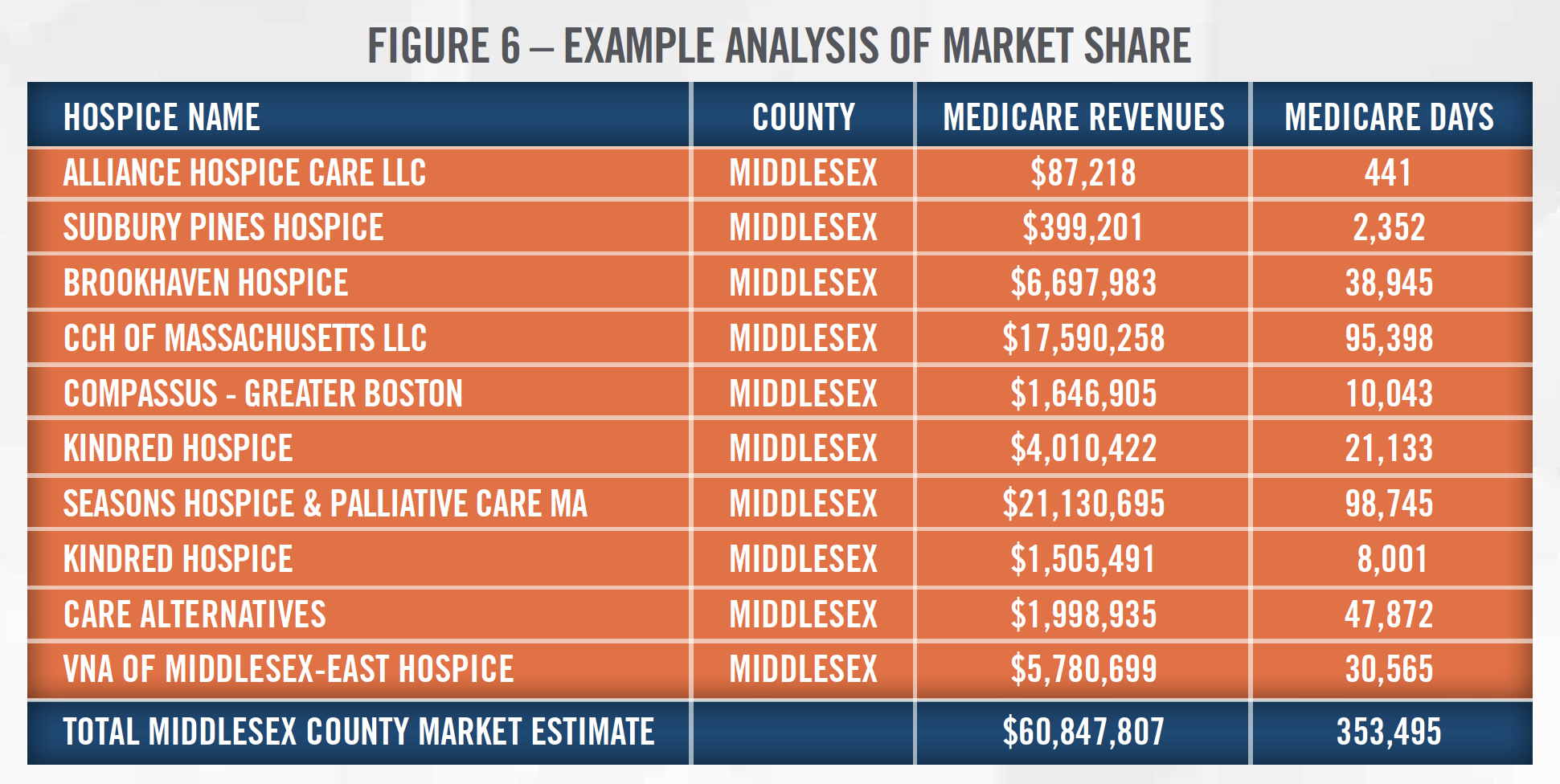

When projecting future financial results for home health and hospice agencies, valuators have many tools at their disposal that can be utilized to help inform the accuracy of the projection. Census data, department of health data (particularly in states with certificate of need requirements), and CMS data can be used to precisely size the market in a particular location and estimate the market share of the providers within that market. Using the market data to assess whether the implied market share they are projecting is reasonable is a necessary step to ensure the defensibility of a valuation conclusion. As an example, Figure 6 presents hospice market share data from Middlesex County, Massachusetts.

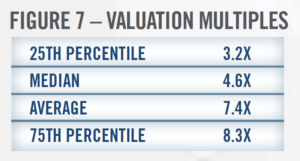

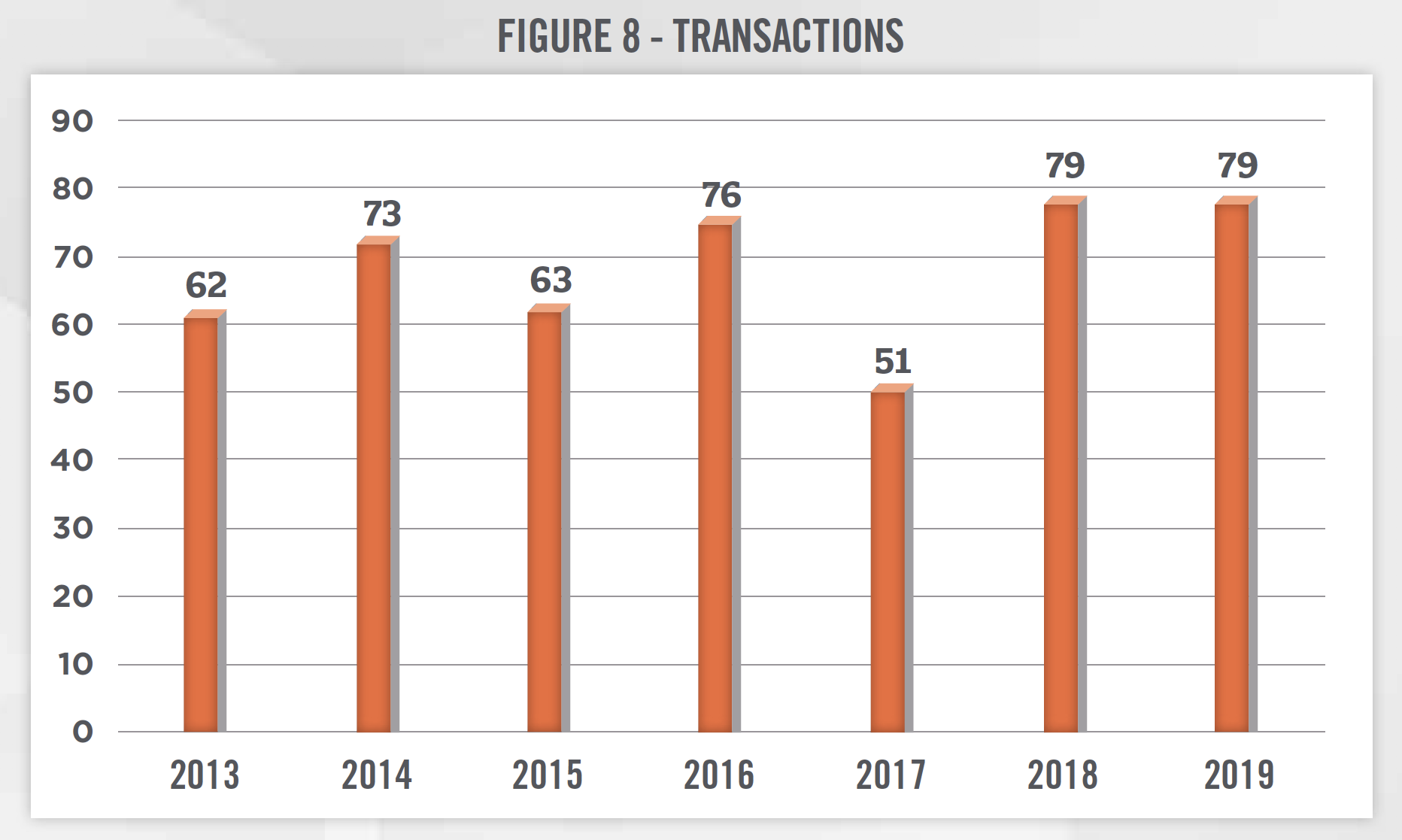

The market approach provides an indication of value by drawing reference to prices paid in transactions involving similar companies, or for shares in publicly-traded companies involved in the same line of business as the entity being valued. There have been many transactions in the home health and hospice sector in recent years that valuators can analyze, and these transactions provide context and an indication of the market multiples paid in the space. Figures 7 and 8 present market value of invested capital to EBITDA multiples for home health and hospice transactions from 2010 through 2019, according to DealStats, as well as the number of transactions each year, according to Irving Levin Associates.

The market approach provides an indication of value by drawing reference to prices paid in transactions involving similar companies, or for shares in publicly-traded companies involved in the same line of business as the entity being valued. There have been many transactions in the home health and hospice sector in recent years that valuators can analyze, and these transactions provide context and an indication of the market multiples paid in the space. Figures 7 and 8 present market value of invested capital to EBITDA multiples for home health and hospice transactions from 2010 through 2019, according to DealStats, as well as the number of transactions each year, according to Irving Levin Associates.

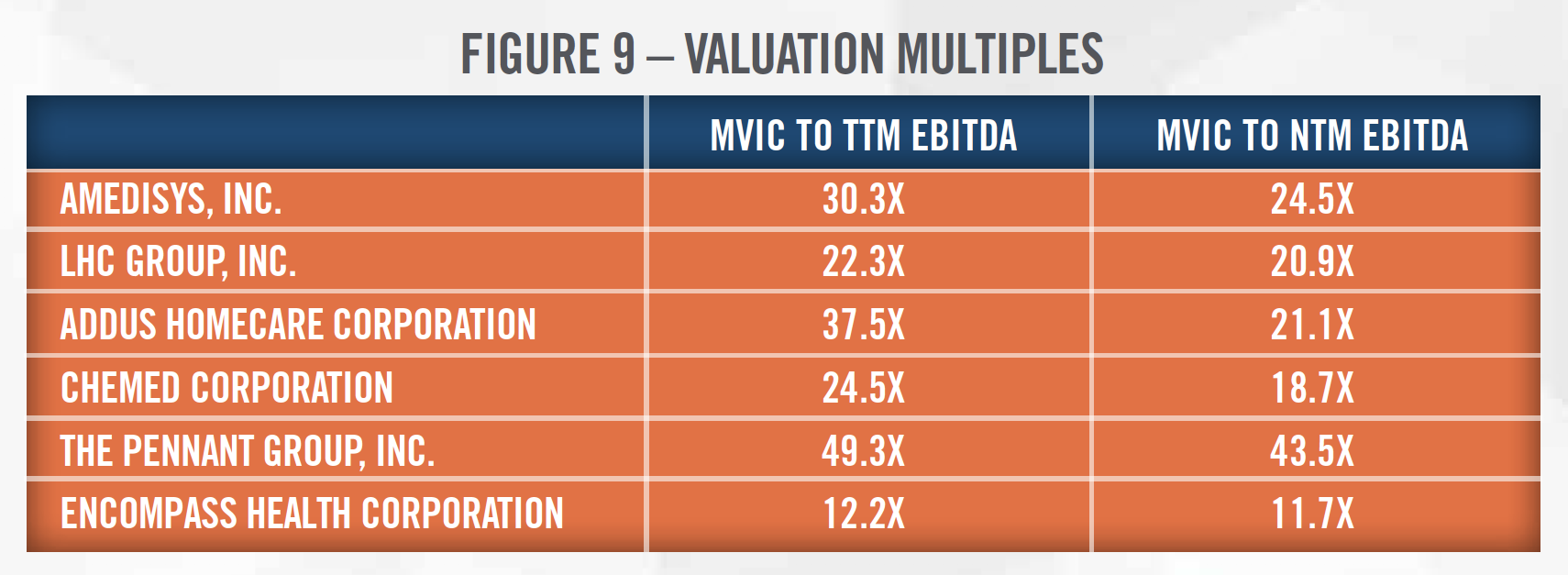

There are also multiple publicly-traded companies that provide home health and hospice services. Figure 9 presents the valuation multiples of the publicly-traded companies in the home health and hospice space as of December 31, 2019. When analyzing these companies and applying the valuation multiples to a subject home health and hospice provider, there are several considerations for valuators to be aware of. Most of the public companies below provide other services in addition to home health and hospice care, so they may not be perfectly comparable to the entity being valued. In addition, the public companies benefit from economies of scale and geographic diversity that make them less risky investments than a home health and hospice agency with fewer providers and geographic service areas. The valuator must consider the specific facts and circumstances surrounding the entity being valued and make adjustments to the multiples before applying them to a subject entity’s EBITDA.

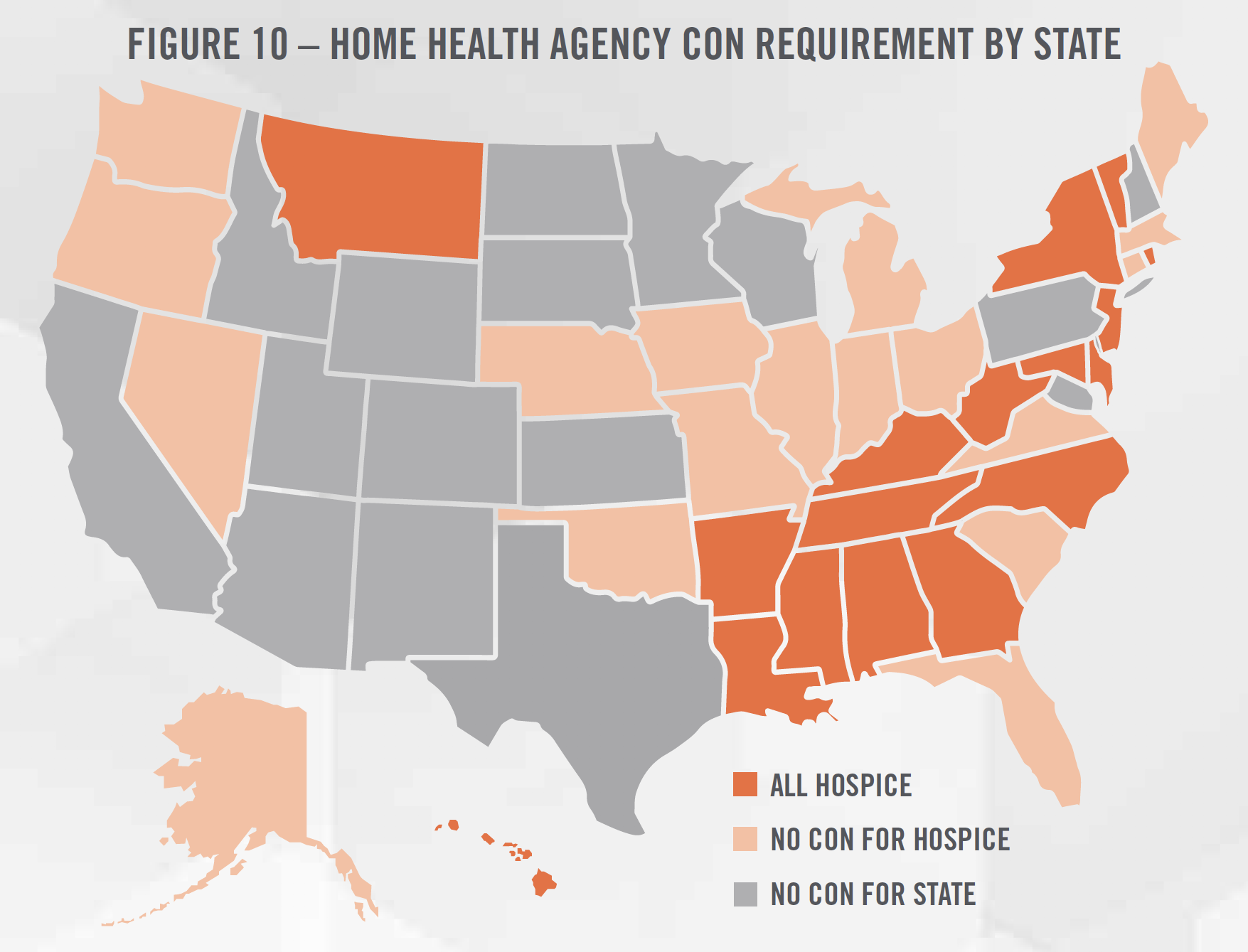

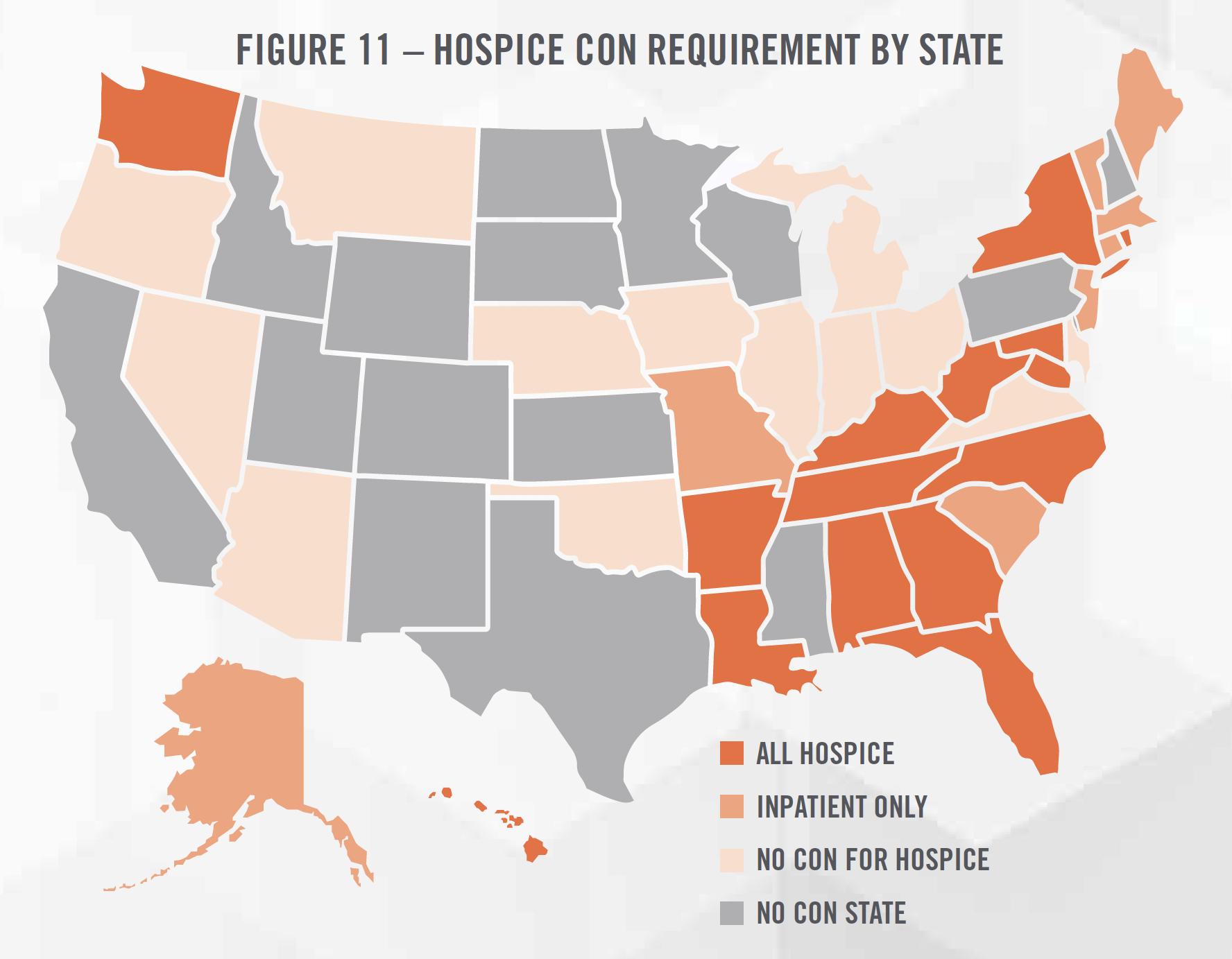

The final approach to consider when valuing home health and hospice agencies is the cost approach, which provides an indication of value based on the cost to recreate the business or asset at todays prices, less economic obsolescence. Given the nature of home health and hospice services, most businesses in the space do not have significant amounts of fixed assets. However, there are a number of intangible assets that can be valued under the cost approach that may be appropriate for valuators to consider. One such asset is a certificate of need (“CON”), which some states require operators to obtain before opening for business. Figures 10 and 11 summarize the CON requirements for each state across the United States.

In addition to the CON, there are other licenses and accreditations that require time and resources to obtain that may represent intangible assets for a home health and hospice business. These agencies also incur expenses associated with recruiting and hiring the workforce necessary to provide services. The existence of a turnkey operation represents an intangible asset for the buyer of a home health and hospice business.

![]() CONCLUSION

CONCLUSION

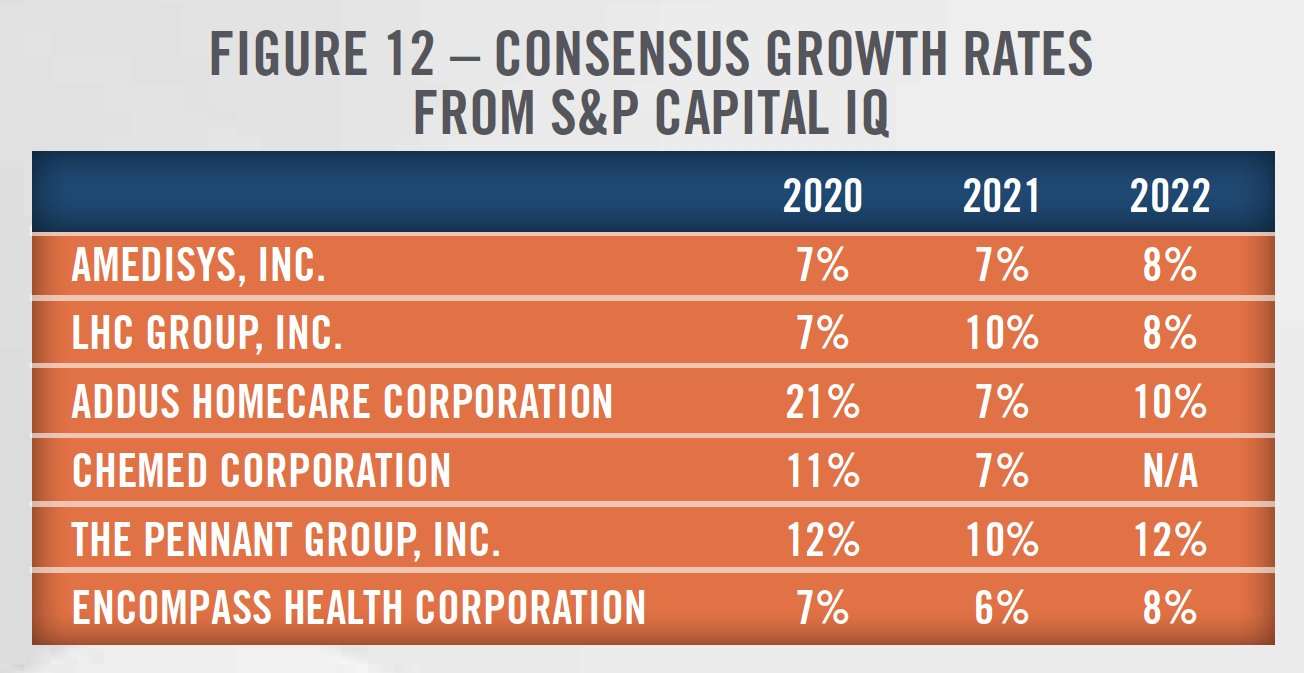

The home health and hospice industries are likely to experience dramatic change in the coming years as Medicare Advantage plans potentially cover hospice services and PDGM is implemented in the home health space. We expect to see a wave of consolidation in home health as smaller operators struggle with the new payment model, including elimination of RAP. Increasing focus on patient satisfaction, increasing use of technology and telehealth, and reducing the cost of healthcare should provide tailwinds to home health providers. Operators in the home health and hospice space should also benefit from the aging population. Overall, the environment will likely be challenging for smaller providers, but larger operators should benefit from strong growth as indicated in the government projections above and the projected growth rates[12] for the public companies presented in Figure 12.

These changes are important considerations and potential influences to the valuation of home health and hospice agencies. HealthCare Appraisers is monitoring the changes and is ready to assist in valuation of these businesses in a dynamic market.

[1] Figures include free-standing and hospital-based Hospices and HHAs that filed cost reports in 2018.

[2] Medpac.gov

[3] CMS analyzed healthcare expenditures based on funding sources as well as site of service. Therefore, healthcare expenditure data for home healthcare will include hospice spending that takes place in the home of the patient, but does not include hospice spending taking place in a nursing facility, hospital, or any other clinical setting.

[4] https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2019.00529

[5] Medpac.gov

[6] https://risk.lexisnexis.com/insights-resources/research/top-100-hospice-and-home-health

[7] https://homehealthcarenews.com/2020/03/home-health-home-care-ma-activity-is-business-as-usual-for-now/

[8] https://homehealthcarenews.com/2020/01/the-top-home-health-trends-of-2020%ef%bb%bf/

[9] https://www.healthcaredive.com/news/home-health-agencies-expanding-rolling-out-more-telehealth-services/568320/

[10] https://mhealthintelligence.com/news/cms-finalizes-new-reimbursement-rules-for-remote-patient-monitoring

[11] https://mhealthintelligence.com/news/current-and-future-doctors-are-more-than-ready-to-use-mhealth-wearables

[12] Represents the average projected revenue growth rates from investment analysts covering the home health and hospice space. Estimates are compiled by S&P Capital IQ.