More than ever, hospital/physician alignment strategies that foster cooperation and shared goals between hospitals and their medical staffs are paramount in achieving quality and efficiency improvements. Unfortunately, looking back historically, many hospitals have not effectively partnered with their medical staff physicians in the planning, management and oversight of their clinical service lines. While medical director arrangements are intended to accomplish these goals, there are significant limitations to the medical director model. First, a relatively small number of physicians are typically “bought in” to the process via their individual medical director roles. Further, medical director agreements usually focus on hours worked rather than results achieved.

The objective of this article is to provide insight into some of the more common issues encountered in the development, implementation and valuation of co-management arrangements.

THE IMPETUS FOR THE SERVICE LINE CO-MANAGEMENT ARRANGEMENT

To address many shortcomings of the medical director model, hospitals are increasingly turning to the concept of clinical service line co-management arrangements. The purpose of these arrangements is to:

1) Involve a larger number of medical staff physicians in the management/improvement process;

2) Redirect the focus of the physicians’ administrative services from an hourly-based arrangement to an objectives-based arrangement; and

3) Encourage achievement of pre-identified goals through incentive compensation.

The form of these arrangements can vary significantly based on the specific circumstances, needs and opportunities of a particular hospital’s service line. However, arrangements that reward the achievement of desired clinical outcomes, including the attainment of specific quality metrics and operational efficiencies, can offer a valuable range of benefits to all involved parties.

STRUCTURE OF SERVICE LINE CO-MANAGEMENT ARRANGENTS

Service line co-management arrangements are pay-for-performance programs whereby hospitals engage physicians to manage and improve entire hospital service lines (e.g., cardiovascular, orthopedics, etc.). Under this type of arrangement, a hospital enters into a formal agreement with certain of its medical staff physicians to manage a designated hospital service line. The primary purpose is to align physician and hospital objectives while recognizing and appropriately rewarding participating physicians for their efforts in managing and improving the overall quality and efficiency of the service line.

The core elements of these arrangements are built on the belief that well-defined operational goals can be achieved when physicians and a hospital work collaboratively. Therefore, these incentive-based management programs are designed with very specific objectives and clearly defined metrics.

TYPICALLY, SERVICE LINE CO-MANAGEMENT ARRANGEMENTS INCLUDE:

- A Base Fee: which is a fixed payment, typically paid monthly, that provides compensation for the day-to-day time and effort of the participating physicians in overseeing, managing and improving the service line.

- An Incentive Fee: which can be paid in whole or in part to the extent that pre-determined service line objectives are met.

Frequently, the co-management organization manages the overall service line as well as its subservice lines, which can result in a very robust arrangement. Using cardiology as an example, sub-service lines might include (i) medical cardiology; (ii) interventional cardiology; (iii) electrophysiology; (iv) cardiac surgery; (v) vascular surgery; (vi) cardiac rehabilitation; and (vii) multiple outpatient centers and clinics.

SERVICE LINE CO-MANAGEMENT ARRANGEMENTS MAY BE STRUCTURED IN ONE OF THE FOLLOWING THREE WAYS:

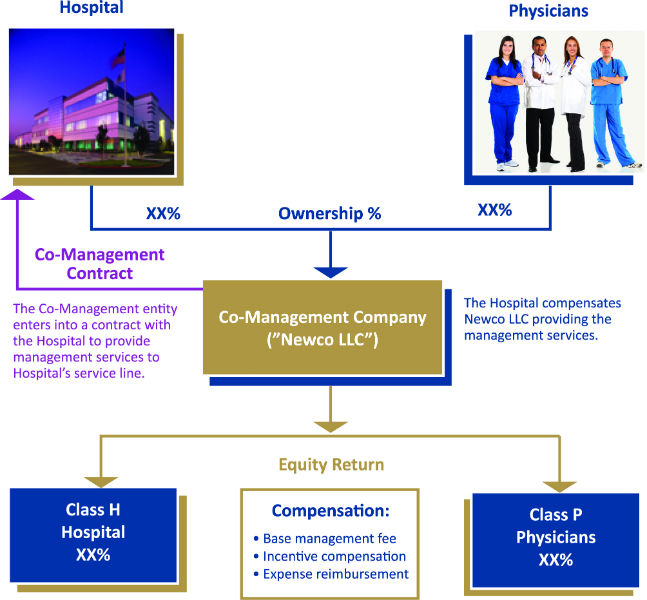

1) A new joint-venture entity (e.g., an LLC) is created consisting of both the hospital and participating physicians as investors. See Diagram 1.

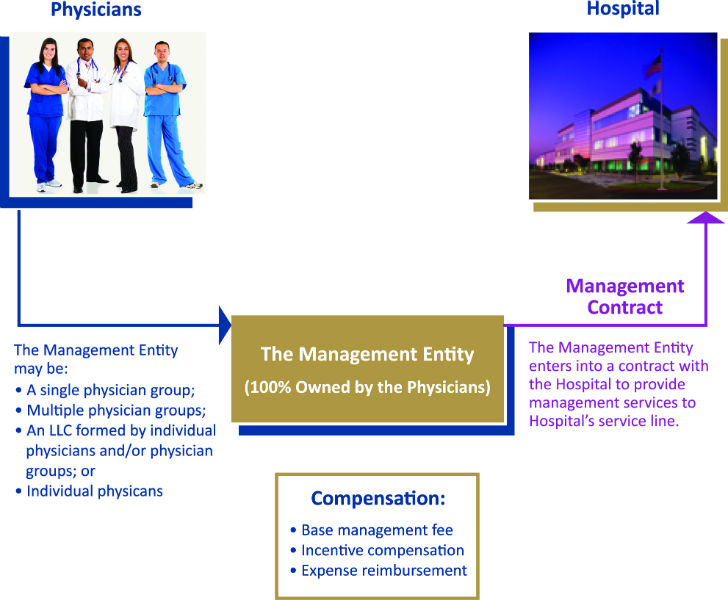

2) A new joint-venture entity is created consisting solely of participating physicians as investors. This newly created physician-owned entity allows physicians from a number of professional practices to have a single contracting entity for purposes of the service line co-management arrangement. See Diagram 2.

3) No new entity is created. The service line co-management is entered into between the hospital and a single physician group practice.

DIAGRAM 1: SERVICE LINE CO- MANAGEMENT WITH A JOINT VENTURE

The co-management structure diagrammed above is intended to be a vehicle to ensure the active participation of the hospital and physicians in the provision of service line management services (i.e., the service line co-management arrangement), whereas the structure in Diagram 2 illustrates the management company as solely owned by physicians (i.e., the service line management arrangement). The key distinction between the two (other than the obvious ownership, governance and capitalization issues) is that in the co-management structure, the resulting division of responsibilities within the co-management company (i.e., the management contribution of each party related to providing the management services), is assumed to be in approximate proportion to the actual ownership percentages.

DIAGRAM 2: SERVICE LINE MANAGEMENT WITHOUT A JOINT VENTURE

DETERMINATION OF FAIR MARKET VALUE: EVOLVING ISSUES

The increasing popularity of co-management arrangements, coupled with the unique dynamics of each individual hospital, has led to greater variation in structure and application.

As such, the arrangements:

(i) Are being implemented for a broad range of service lines;[1]

(ii) May represent only one of several arrangements between the hospital and the physician group[2] or individual physicians;[3] and

(iii) Must be established with some consideration to tracking the actual performance of co-management tasks and incentives.[4]

5 KEY FACTORS TO CO-MANAGEMENT FMV

Therefore, the determination of the fair market value (“FMV”) of compensation for the co-management arrangement[5] must consider and address the totality of the arrangement, including the following five key factors:

1) OTHER ARRANGEMENTS THE HOSPITAL MAY HAVE WITH THE PHYSICIAN(S)

There is a small but increasing trend to utilize hospital-employed physicians as managers within service line co-management arrangements. Regardless of the underlying employment model, it is important to realize that the employment relationship adds to the complexity of the co-management arrangement, as the hospital now needs to be concerned with the aggregate compensation (or potential compensation) of its employed physicians. To help mitigate this concern, when employed physicians become ”co-managers,” the co-management agreement should clearly state that the base and incentive management tasks and responsibilities are performed in addition to the services required within the physician’s employment arrangement.

Furthermore, issues related to the allocation of time between the different arrangements can become problematic when the employment arrangement is time-based[6] (e.g., shift coverage), as opposed to productivity-based.[7] In these cases, mechanisms for tracking and documenting time spent performing required duties should be incorporated into the structure of at least one of the arrangements.[8] Regardless, the hospital and its valuation firm need to consider the “totality” of the potential compensation, including the possibility that the physician has now overcommitted him/herself to a basket of duties that are not achievable.

2) THE METHODOLOGY USED TO TRACK AND COMPENSATE THE ACHIEVEMENT OF THE DAY-TO-DAY MANAGEMENT TASKS

Since a vast number of co-management arrangements are focused on a task-based compensation model[9] to earn the base or fixed portion of the compensation (i.e., base management tasks), tracking and documenting actual task achievement needs to be carefully addressed. Task-tracking methodologies can vary widely in terms of approach, practicality and validity, and as such, a comprehensive task-tracking plan should be developed in parallel with the creation of the co-management arrangement.

It should also be noted that base management tasks need to be reviewed on an annual basis to ensure that they are relevant and appropriate. For example, if a base management task relates to the development of patient educational materials, it would likely follow that after the agreement has been in place for a year, this task should be updated or eliminated. Similarly, performance based metrics associated with the payment of incentive compensation also require updating at the end of each year of the agreement, such that the applicable metrics are “reset.”

3) THE SCOPE AND BREADTH OF THE HOSPITAL’S SERVICE LINE BEING MANAGED

Service line net revenue (commonly referred to as net collections) is a key element considered within the framework of a FMV analysis for service line management arrangements. Therefore, the determination of net revenue is a critical part of the data collection process.

In most cases, net revenue is based on MS-DRGs and ICD-9 codes, depending on whether the services we provided to inpatients or outpatients. For well defined service lines, like orthopedic surgery, MS-DRGs and ICD-9 codes are readily identifiable as belonging to orthopedics, therefore, allowing relevant net revenue information to be easily ascribed to a particular service line. However, for other service lines, including primary care,[10] the identification of service line specific net revenue becomes problematic. Since primary care is often included in the treatment of all inpatients, regardless of their primary diagnosis, it becomes almost impossible to determine that portion of net revenue associated with primary care for a patient whose primary MS-DRG relates to a particular medical specialty (e.g., hip replacement).

Furthermore, service line co-management arrangements are based on the management of a specific clinical service line (e.g., orthopedic surgery), and therefore, do not easily accommodate managers from different service lines (e.g., it would be difficult for a primary care co-management company to assume management responsibilities for the orthopedic service line). Therefore, within an orthopedic service line, the overall management of joint replacement patients is the responsibility of the orthopedic surgeons performing the surgery, even though a primary care physician may have seen and even provided treatment to the patient. Therefore, when determining net revenue associated with a primary care service line, only selecting MS-DRG and ICD-9 codes specifically associated with primary care patients will result in a more conservative revenue calculation, as it won’t include services coded for other service lines (e.g., orthopedic surgery).

4) THE IMPACT OF PAYOR MIX AND SOURCES OF REVENUE

As with other analyses using patient net revenue as a variable, the determination of FMV of a management arrangement may be significantly impacted by the service line’s payor mix. For example, when a co-management arrangement is developed for a service line that includes a high percentage of poor payors,[11] the hospital and its valuation firm should consider making certain adjustments in order to appropriately “normalize” the negative impact of poor payors on the determination of the FMV range.[12] Alternatively, it is common for a valuation firm to also undertake a cost approach in its analysis, and since such approach does not rely on net revenue in its application, an “averaging” of the two approaches’ resulting ranges will further help to mitigate the effects of a high poor payor mix.

5) THE INTEGRATION OF DESIGNATED MEDICAL DIRECTORS AND/OR A SERVICE LINE ADMINISTRATOR

Service line co-management arrangements include specific requirements for the management of tasks related to the general day-to-day operation of the service line. These base management tasks[13] often include, among others, requirements to:

(i) Oversee, train and direct staff;

(ii) Develop clinical and operating protocols;

(iii) Develop benchmarks and best practices; and

(iv) Monitor patient, staff and physician satisfaction.

Therefore, care must be taken to ensure that there are no compensated individuals providing services substantially similar to service line management tasks and responsibilities (e.g., traditional hospital medical directors and/or service line administrators). If there are, the hospital and its valuation firm need to ensure that such compensation arrangements are either terminated or modified such that they become an expense payable from the base management fee.

MEDICAL DIRECTORS

As previously indicated, service line co-management arrangements are generally created to improve operations and achieve identified outcomes and standards. Within this paradigm, the management entity[14] is responsible for performing a comprehensive list of management tasks (the basis for the base management fee), as well as for achieving certain performance-based metrics (the basis for the incentive management fee).

Similarly, hospital-based medical directors have traditionally been engaged to provide certain service line-related management and administrative tasks.

Therefore, it becomes of significant importance to determine whether there is any “overlap” of the duties and responsibilities of the manager and the medical director(s). Unfortunately, in our experience, there is generally a significant degree of overlap in the administrative and management tasks required of the manager and the medical director(s). As such, medical director(s) who are responsible for performing a subset of the management tasks, must be compensated from the base management fee paid to management entity.

For example, the orthopedic surgery co-management entity is responsible for the management of all orthopedic surgery service line activities. Therefore, should the hospital also wish to continue maintaining a traditional medical director of joint reconstruction and replacement, such position needs to be compensated from the base management fee in order to avoid any FMV implications.

THE SERVICE LINE ADMINISTRATOR

Similar to the discussion above related to a medical director, a service line administrator is often engaged to perform services in conjunction with a service line management arrangement. As with the medical director, if the service line administrator is responsible for performing tasks similar to those required of the co-management company, then the administrator must be compensated as an expense from the base management fee.

Notwithstanding, in an increasing number of management arrangements, the administrator is an employee of the hospital and is responsible for overseeing the hospital’s interests in terms of service line management, rather than actually providing any of the management services. In these cases, since the administrator does not have any responsibility for performing specified management services, the administrator would not be required to be compensated from the base management fee.

SUMMARY

The emergence of incentive-based models for the delivery of healthcare services has contributed to the development of a broad range of evolving opportunities for hospital-physician partnerships. One of the most promising forms of these partnerships involves the establishment of a co-management company for the purpose of managing a specific hospital service line. As they grow in popularity, these types of arrangements continue to increase in complexity, resulting in the emergence of new issues which require consideration in the valuation process.

[1] In our experience comprehensive cardiovascular and orthopedic surgery co-management arrangements are currently the most prevalent, due to the inherent range and complexity of their subservice lines. However, as the co-management vehicle grows in popularity, we have also witnessed increases in the number of management arrangements involving the following service lines: (i) surgical services; (ii) gastroenterology; (iii) hematology/oncology; (iv) wound care centers; and (v) sleep clinics.

[2] As in the case of on-call arrangements with the physician group(s).

[3] As in the case of employed physicians.

[4] Base management tasks as well as incentive-based performance metrics must be tracked to document their achievement.

[5] Including both the base and incentive fees.

[6] Compensation models based on productivity are not impacted by this issue, as the compensation associated with their employment is based on the actual performance of clinical procedures.

[7] If the underlying employment arrangement is based on productivity (e.g., wRVUs), it may be possible that the two arrangements, acting in concert, become self-normalizing. For example, if the physician spends a disproportionate amount of time on management duties, it is likely that clinical productivity (and therefore compensation for clinical services) will decrease.

[8] Since one of the significant attributes of the co-management model is its reliance on “task-based” versus “time-based” compensation, it would seem likely that a time-tracking mechanism for the employment arrangement would be the most beneficial approach to reducing problems related to redundant payments.

[9] Payment is made based on the completion of certain defined tasks, regardless of the amount of time required to complete them.

[10] Primary care generally includes internal medicine, family medicine and general practice medicine.

[11] Typically defined as Medicaid, self-pay and charity care.

[12] From our perspective, we do not believe that a service line co-management company should be unfairly penalized in terms of the management fee simply because the hospital experiences a high percentage of poor payors in its patient population. The amount of work required to effectively manage service lines of comparable size, with respect to patient volume and procedures performed, is similar and does not depend on the payor mix.

[13] These base management tasks, which involve the day-to-day management of the service line, are different from the incentive management tasks, which typically involve the achievement of specified performance metrics involving, but not limited to, operational, patient satisfaction and/or new program initiatives.

[14] The joint venture, in the case of a co-management arrangement, and the physicians and/or physician entity, in the case of a management company.